Microloans

There is enormous potential in providing additional financial services in emerging economies, but they come with peculiar issues too. The problem of low repayment rates remains unsolved except where strict selection processes or good enforcement mechanisms exist.

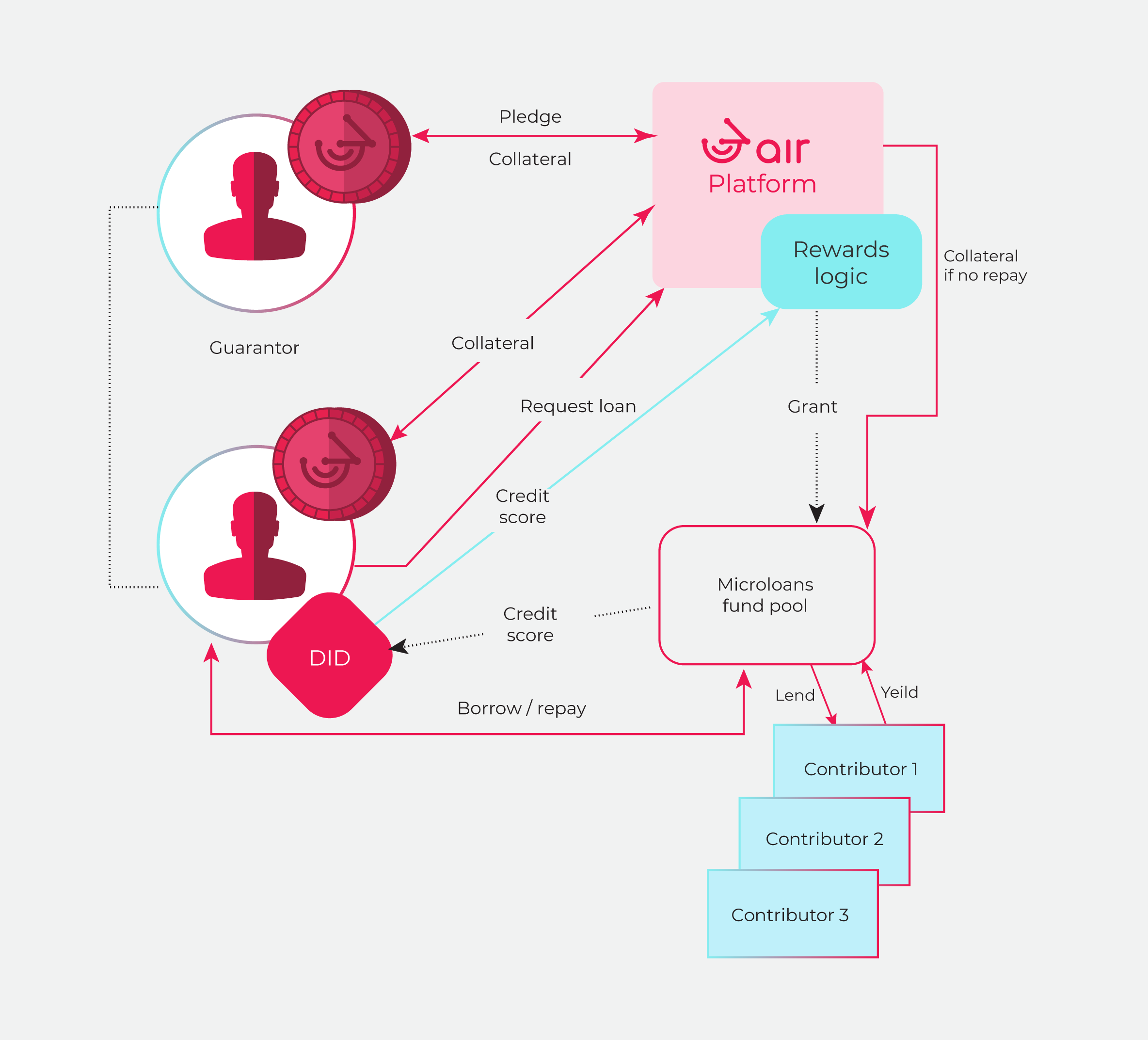

As a platform for ISP providers and a DID issuer, we will be exploring the options of providing microloans to customers for acquired services. With a valid payment track record and other personal information, we can enter low-risk microloans in the scope of previously acquired services. Additionally, 3air tokens can be staked as collateral for loan repayment.

With time, a large amount of data should enable us to build a sound credit score model that could potentially allow the 3air platform to expand microloans beyond the ISP providers, giving customers options for financial inclusion and standard banking services. A working microloans system could attract external capital into emerging economies to facilitate faster growth. A good system could also facilitate undercollateralized loans in the future.

A special team will be assigned to the area of general microloans system development, focusing on anonymous analysis of data collected from ISPs with the purpose of building advanced AI algorithms for autonomous microloans processing and approval.

We will build upon experience of existing projects such as Kiva and published academic papers1.

3air will devote resources and form a special team to research microloans and seek partnerships with current leaders in this field. A separate whitepaper on the subject of microloans may be published at a later stage.

Figure 18 3air microloans system

1 Papers like Tchakoute-Tchuigoua and Soumaré: The effect of loan approval decentralization on microfinance institutions outreach and loan portfolio quality and Dushimimana, Wambui, Lubega and McSharry: Use of Machine Learning Techniques to Create a Credit Score Model for Airtime Loans